Office Market in Balance?

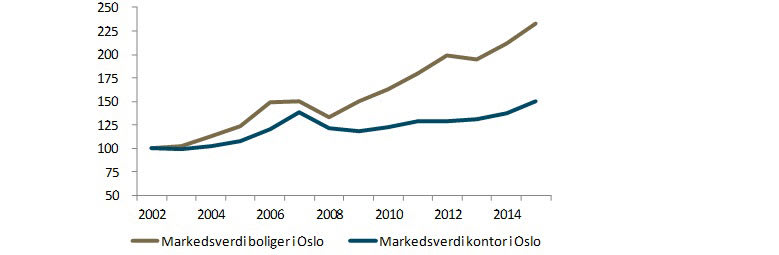

Since 2002, housing prices in Oslo have increased by 133 percent, while the value of office buildings has risen by 50 percent. The office rental market appears to be accommodating Oslo’s new residents much more effectively than the housing market.

The Norwegian economy has experienced a golden age. High economic growth, strong population growth and decreasing interest rates are a potent combination that is continuously lifting the property market to new heights. However, there has been a major difference in the growth in value between residential properties and office properties. The graph below illustrates the increase in value of residential and office properties in Oslo since 2002.

Keep in mind that these are average figures and there are significant variations between areas within each segment. It should also be noted that growth in value is not the same as the return, because rental incomes have not been included.

An area can be used for housing, offices or other activities. Housing and offices thus compete for the same space. It is therefore remarkable that the development in value between these two segments has been so vastly different.

Source: Eiendom Norge/Finn/Eiendomsverdi/MSCI IPD/UNION

A report from the OECD stated that there is very little price elasticity in the Norwegian housing market compared with other well-developed countries. This means that the supply side reacts slowly to price changes. In a well-functioning market, a significant price rise will result in more providers entering the market and increasing the volume which will then normalise the profit. In this way, market forces push the price back into balance. According to the OECD, this dynamic is weak in the Norwegian housing market.

The reasons for why the supply side in the housing market does not appear to function in an optimal manner are unclear. However, the consequence of an inelastic market is obvious, i.e. there is a greater risk that the market will fall out of balance.

Why has the increase in value of office buildings been much more moderate? The most important explanation is that enough office space has been built. Office vacancy rates are presently at around eight percent. At the same time, unemployment is low, something that must mean that the majority of new Oslo residents have found work. In other words, the supply side in the office rental market is relatively efficient, albeit not without cyclical fluctuations.

The twofold development is largely made possible by two barriers. Firstly, politics and regulations guide the development. Secondly, there are considerable conversion costs associated with converting buildings for different use. Despite this, we are now seeing an increasing number of office buildings being converted into housing. Together with limited new construction of offices in the coming years, this will contribute to balancing out the office rental market during a challenging period.